When you're on Medicare Part D or any prescription drug plan, your out-of-pocket costs for medications don't just depend on the drug itself - they depend on which tier it's in. And those tiers can change without warning. Every year, insurance plans update their formularies - the official list of drugs they cover - and move medications up or down in cost tiers. For seniors taking multiple prescriptions, even a small shift in tier can mean hundreds of extra dollars a year. Knowing how to check these changes isn't just helpful; it’s essential to avoid surprise bills.

What Is a Drug Formulary and How Do Tiers Work?

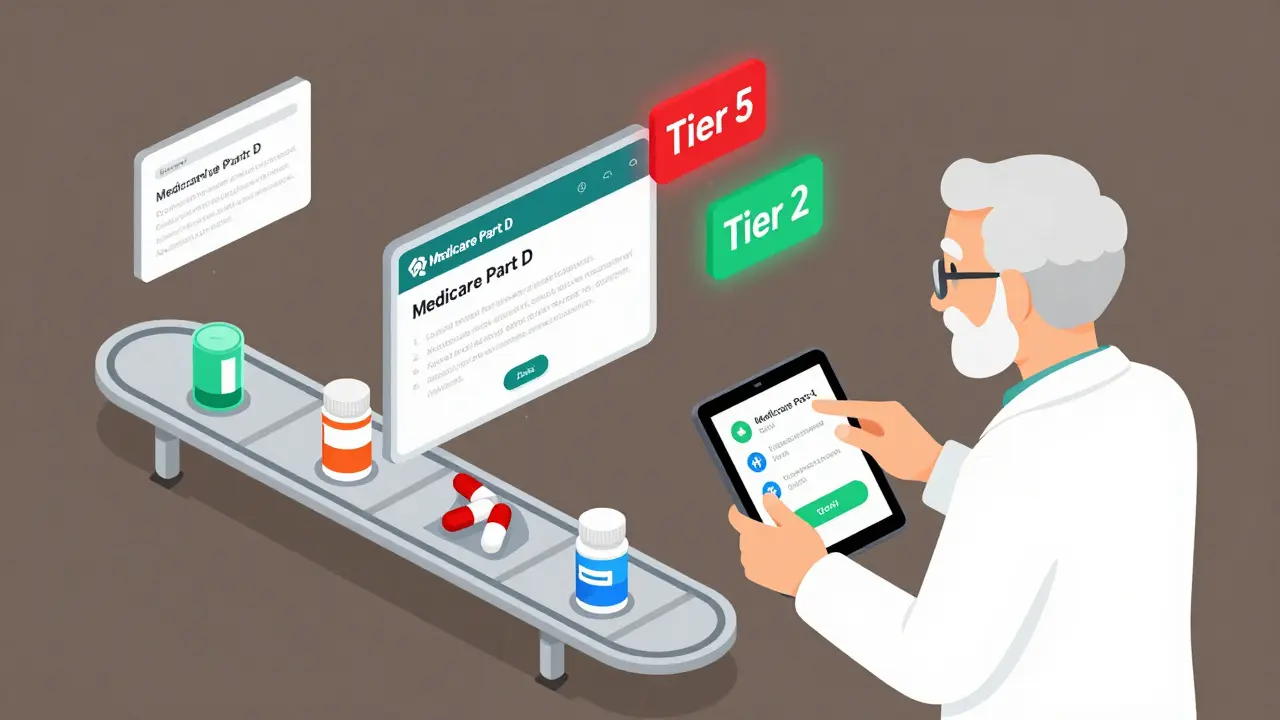

A drug formulary is simply the list of medications your plan covers. Not every drug is included, and even if it is, the cost you pay depends on its tier. Most plans use a 3-tier, 4-tier, or 5-tier system. Here’s how they typically break down:- Tier 1: Preferred generics - lowest cost, often $0-$10 copay

- Tier 2: Non-preferred generics or lower-cost brand-name drugs - around $15-$30 copay

- Tier 3: Higher-cost brand-name drugs - $40-$70 copay

- Tier 4: Non-preferred brands or specialty drugs - $80-$150 copay

- Tier 5: Specialty medications - often over $200, sometimes coinsurance (like 33% of the drug cost)

For example, if your blood pressure medication is in Tier 1, you might pay $10 a month. If it moves to Tier 3 next year, that same pill could cost you $55. That’s not a typo. And it happens more often than people realize.

Why Do Formularies Change?

Changes aren’t random. They’re driven by real-world factors:- A new generic version of a brand-name drug hits the market - the plan moves the old brand to a higher tier to push people toward the cheaper generic

- New safety data emerges - if a drug is linked to more side effects, the plan may restrict it or raise the cost

- Drug prices rise - especially for specialty drugs like GLP-1 weight loss medications (Wegovy, Ozempic), which are increasingly being moved into Tier 4 or 5

- Plan negotiations with drugmakers - if a manufacturer stops offering discounts, the plan may bump the drug to a higher tier

According to CMS data, about 17% of formulary changes in 2023 involved moving a drug to a higher tier, increasing what you pay. And it’s not just Medicare - private insurers do the same.

How to Check Your Drug’s Tier and Coverage

The easiest way to check your coverage is through your plan’s online formulary tool. Here’s how:- Go to your insurance provider’s website - for Medicare Part D, that’s usually your plan’s portal (like Humana, Cigna, or Excellus BCBS)

- Find the "Drug Formulary" or "Drug List" tool - it’s often under "Benefits," "Prescriptions," or "Member Resources"

- Search for your medication by name - use the brand name or generic name (both work)

- Look at the tier it’s listed under and the associated cost - this will show your copay or coinsurance

- Check the "Notes" section - it may say if prior authorization, step therapy, or quantity limits apply

Most tools update on January 1st each year, but changes can happen anytime. If a drug you’re taking gets moved to a higher tier, your plan is required to notify you - usually by mail or email - at least 60 days before the change takes effect. But don’t wait for them. Check your drugs yourself every fall before open enrollment, and again in early spring.

What If Your Drug Isn’t Covered or Got Moved Up?

If your medication suddenly isn’t on the formulary or got bumped to a higher tier, you have options:- Ask your doctor for an alternative - there may be another drug in the same class that’s covered at a lower tier. For example, if your brand-name statin moved up, your doctor might switch you to a generic like atorvastatin.

- Request a formulary exception - you can ask your plan to cover your drug even if it’s not on the list. You’ll need your doctor to submit a letter explaining why the alternative drugs won’t work for you. In 2022, about 68% of these requests were approved, according to CMS.

- Use a 30-day transition supply - if your drug was removed or moved, your plan must give you at least one 30-day refill while you and your doctor figure out next steps.

One user on Medicare.gov shared: "My diabetes drug was moved from Tier 1 to Tier 3 overnight. I called my pharmacist - they found a similar drug in Tier 2 that my doctor approved. I saved $45 a month."

Common Mistakes Seniors Make

Many seniors don’t realize how easily formularies can impact them. Here are the top three mistakes:- Assuming last year’s coverage = this year’s coverage - even if you stayed with the same plan, your drugs may have moved tiers

- Not checking during open enrollment - between October 15 and December 7, you can switch plans. Use this time to compare formularies

- Ignoring notices - if you get a letter saying "Your drug list is changing," don’t toss it. Read it. Call if you’re unsure

GoodRx found that 42% of formulary-related calls to customer service come from seniors who didn’t check their coverage until after they were charged more at the pharmacy.

Tools and Resources to Help

You don’t have to figure this out alone. These free tools exist to help:- Medicare.gov’s Plan Finder - enter your drugs, zip code, and pharmacy. It compares formularies across all Part D plans in your area

- SHIP Programs - State Health Insurance Assistance Programs offer free one-on-one counseling. In 2022, they helped over 1.7 million seniors with formulary questions

- Pharmacist consultations - your pharmacist can check your formulary, suggest alternatives, and even help you file an exception request

- GoodRx and SingleCare - these apps show cash prices and sometimes beat your insurance copay

UnitedHealthcare and Cigna score high in clarity for their formulary tools, according to J.D. Power’s 2023 report. Smaller regional plans? Not so much. If the website is confusing, call them. Customer service is required to answer your questions.

What’s Changing in 2026?

The landscape is shifting fast. GLP-1 medications for weight loss - once mostly covered in lower tiers - are now being moved into specialty tiers, sometimes costing over $1,000 a month. Plans like FepBlue have admitted that some 2026 drug lists still show these drugs in the wrong tier, meaning changes are still being made.CMS is testing a simplified 4-tier model for 2025 to reduce confusion. But until then, the rules stay complex. Also, by 2026, over half of the top-selling drugs are expected to be specialty medications - meaning more seniors will face higher-tier costs.

One thing won’t change: if you don’t check your formulary, you’ll pay more. And you won’t know why.

How often do drug formularies change?

Formularies are updated annually on January 1st, but changes can happen mid-year. Plans must notify you 60 days in advance if they remove a drug or add new restrictions - except in cases of safety concerns, where changes can happen immediately. Always check your plan’s website in late fall and early spring.

Can I switch plans if my drug is moved to a higher tier?

Yes - during Medicare’s Annual Enrollment Period (October 15 to December 7), you can switch to a different Part D plan that covers your drugs at a lower tier. You can also switch during a Special Enrollment Period if you lose other coverage or move out of your plan’s service area.

What’s the difference between a copay and coinsurance?

A copay is a fixed amount you pay - like $15 for a Tier 1 drug. Coinsurance is a percentage of the drug’s total cost - for example, 33% of a $300 specialty drug means you pay $100. Tier 5 drugs usually use coinsurance, which can make costs unpredictable.

Do all Medicare Part D plans have the same formulary?

No. Each plan creates its own formulary. The same drug might be in Tier 1 on one plan and Tier 3 on another. That’s why comparing formularies during open enrollment is critical - even if you like your current plan, another one might save you hundreds.

How do I request a formulary exception?

Ask your doctor to fill out a formulary exception request. They’ll need to explain why the drugs on the formulary won’t work for you - for example, if you had side effects or your condition didn’t improve. Submit the request to your plan. You’ll get a decision in 72 hours (or 24 hours for urgent cases). If denied, you can appeal.

James Moreau

March 23, 2026 AT 01:37Just wanted to say this post saved me a ton of money last year. I didn't realize my insulin had moved to Tier 4 until I got the bill. Checked the formulary, found a nearly identical generic on Tier 2, talked to my doctor, and switched. Saved $300/month. Seriously, check your drugs every fall. It's not hard.

Also, don't ignore those mailers. I used to toss them. Now I keep them in a folder labeled "DRUG CHANGES." Best habit I ever picked up.

J. Murphy

March 24, 2026 AT 13:22formularies are a scam

Raphael Schwartz

March 25, 2026 AT 18:21They just wanna make you pay more. All these plans are owned by big pharma anyway. You think they care if you can afford your meds? Nah. They just want your cash. And they got the government on their side. This whole system is rigged.

winnipeg whitegloves

March 27, 2026 AT 17:50As a Canadian who’s watched this mess unfold south of the border, I gotta say - it’s wild how convoluted this all is. We’ve got our own issues, sure, but at least we don’t have to play drug-tier Tetris just to afford our blood pressure pills. I’ve got a buddy in Arizona who switched meds three times in two years because his plan kept moving things around. It’s exhausting.

Also, props to SHIP programs. They’re basically healthcare superheroes in sweater vests.

Rachele Tycksen

March 29, 2026 AT 11:16i always forget to check and then get hit with a $120 bill for my metformin 😭

Grace Kusta Nasralla

March 29, 2026 AT 22:08It's not just about tiers. It's about the erosion of dignity in healthcare. When your life-saving medication becomes a transactional commodity, we've lost something fundamental. The system doesn't see you as a person - it sees you as a data point in a cost-benefit algorithm. And that's not just inefficient. It's spiritually bankrupt.

Aaron Sims

March 31, 2026 AT 16:52Oh, so now they’re gonna "notify" you 60 days in advance? Like, with a POSTCARD? In 10-point font? In the same envelope as your Walmart receipt? And you’re supposed to READ it? HA. I got a letter last year that said "YOUR DRUG IS NOW IN TIER 5" - and the whole thing was printed in Comic Sans. That’s not a notice - that’s a middle finger.

Stephen Alabi

April 1, 2026 AT 13:11It is imperative to underscore that the structural inefficiencies inherent in the current Medicare Part D formulary paradigm are not merely administrative inconveniences - they are systemic failures of fiduciary responsibility. The reliance upon tiered cost-sharing mechanisms, which are predicated upon opaque negotiations between private insurers and pharmaceutical manufacturers, engenders a pernicious asymmetry of information that disproportionately burdens the elderly demographic. Furthermore, the notion that a 60-day notification window constitutes adequate consumer protection is, in fact, a gross misrepresentation of procedural justice. One must interrogate the ethical underpinnings of a system wherein pharmaceutical access is contingent upon bureaucratic compliance.

Agbogla Bischof

April 1, 2026 AT 14:29From Nigeria, I can say this: we don’t have formularies - we have scarcity. If you can find the drug at all, you pay whatever they ask. No tiers. Just "yes or no." So I’m grateful for this system, even with its flaws. At least you have tools to fight back.

Also - use GoodRx. Always. Even if your insurance says "$15," check GoodRx. Sometimes it’s $8. I learned this the hard way after overpaying for my dad’s losartan for six months. Don’t be like me.

Elaine Parra

April 2, 2026 AT 22:51Let’s be real - this whole "check your formulary" advice is just corporate gaslighting. They know you won’t check. They count on it. They move drugs to higher tiers on purpose, then act surprised when you complain. And don’t get me started on "formulary exceptions." You need a law degree and a second mortgage just to file one. This isn’t healthcare. It’s a predatory game designed to extract money from the sick. And they call it "patient empowerment."